U.S. stocks trade near unchanged after the worst day for the S&P 500 since October 2020 as investors weigh an expected ban on imports of Russian oil.

Archive for category: Uncategorized

Here are three ways the Federal Reserve could shrink its near $9 trillion balance sheet as it looks to cool inflation, according to a senior Columbia Threadneedle rates strategist.

Gas prices over $5 a gallon displayed at gas stations in Mill Valley, California, on February 23 amid the escalating conflict between Russia and Ukraine. | Justin Sullivan/Getty Images

Summer driving season is going to suck.

The backdrop of global and domestic inflation in the United States was already worrying. Now, Russia’s invasion of Ukraine and the global reaction to it stand to make the situation worse — including sending gas prices soaring.

The conflict has roiled global markets, causing stock market turmoil, sending oil prices higher, and injecting even more uncertainty into an already off-balance worldwide economy. It’s also sparked concerns that inflation, already running hot, could run even hotter.

In the United States, the Consumer Price Index, which measures the average change in prices consumers pay for goods and services, was up by 7.5 percent over the past year in January. That’s a 40-year high. The hope was that inflation would soon start to come down, and that factors driving it, such as high gas prices and supply chain woes, would finally pass. Now, it appears that the situation could be quite the opposite.

“What we’re observing is essentially an energy price shock and a financial markets shock that comes on the back of this already concerning inflation environment, an environment in which global supply chains are already stressed and in which there is already some degree of uncertainty as to the outlook,” said Gregory Daco, chief economist at EY-Parthenon. “It’s not just a shock in isolation, it’s a shock in that context.”

Russia is one of the biggest oil and gas producers in the world, and any disruptions stand to have a major impact on prices — disruptions we’re already seeing. On Tuesday, President Joe Biden announced that the US would ban imports of Russian oil, natural gas, and coal. The United Kingdom has said it will scrap Russian oil imports as well. These maneuvers prompted a spike in oil prices, which have already been on the rise, and the situation is sure to have ripple effects across the global economy.

In early February, JPMorgan analysts projected that disruptions to oil flows from Russia could push oil prices to $120 per barrel, which, indeed, it already has. (For context, oil was priced in the $60 per barrel range a year ago, and started 2020 in the $70s and $80s.) Some analysts have warned that worst-case scenario oil prices could hit $200, and Russia has warned that $300 oil prices could be on the horizon, depending on what Europe, which is much more reliant on Russian oil and gas than the US, does.

In the US, Russian oil made up about 3 percent of shipments in 2021, according to Bloomberg, and when you include other petroleum products, that rises to 8 percent. That’s not a ton, but it’s not nothing, either. Major oil companies, such as Shell and BP, have said they’ll stop buying oil and gas from Russia and curb business with the country, which is causing volatility and prices changes as well. Europe is starting to move away from its dependence on Russia, too.

Americans — already dealing with high gas prices and annoyed at the rising costs of heating their homes — are in for a bumpy ride. Gas prices matter not just for people filling up the tanks of their cars but also because of shipping and transportation. The conflict could also translate to high diesel prices and jet fuel for airplanes. “The inflation machine is just not going to slow down,” said Patrick De Haan, head of petroleum analysis at GasBuddy.

According to AAA, the average price of gas nationally is $4.17 a gallon, up significantly from $2.66 a year ago. That number now stands to climb even higher, especially as the summer months approach, which will put more people on the road. As the New York Times points out, the last time gas prices were so high was during the 2008 financial crisis, when — adjusted for inflation — a gallon was priced at about $5.37.

Joe Brusuelas, chief economist at accounting and consulting firm RSM, told CNN in February that the Russia-Ukraine conflict could push inflation to 10 percent year over year, driven in part by gas. By his calculation, an increase in oil prices to $110 could increase consumer prices by 2.8 percent over the course of a year. Alan Detmeister, an economist at UBS, told the New York Times that oil at $120 per barrel could mean inflation at 9 percent in the coming months.

“It becomes a question of: How long do oil prices, natural gas wholesale prices stay elevated?” he told the Times. “That’s anybody’s guess.”

In remarks at the White House on Tuesday, President Biden acknowledged that the Russia-Ukraine conflict and measures the US and Europe have taken to push back against Russia will be felt domestically. “This decision today is not without cost here at home,” he said, referring to the Russian oil ban.

The Biden administration has promised to try to protect Americans from a spike in gas prices. Over the weekend, Secretary of State Anthony Blinken told CNN that the US is “talking to our European partners and allies to look in a coordinated way that prospect of banning the import of Russian oil while making sure that there’s still an appropriate supply of oil on world markets.”

Still, the options on oil supply are limited, at least in the immediate term. “The president has insinuated that he’s got it, he’s going to do everything he can,” said De Haan in February, but it’s not clear what other strings Biden can pull on. Striking a new nuclear deal with oil producer Iran could help, but it’s no silver bullet, nor is it clear it’s very likely to happen. “It’s no Russia, in terms of oil supply,” De Haan said. The US has also begun weighing whether it could look to Venezuela.

Higher oil prices could dampen on economic growth. People and companies having to spend more on oil and gas could reduce spending in other areas, and that could cut into GDP. By one estimate, a long-term increase in gas prices could cost the typical household in the US $2,000 per year.

There are other areas where the Russia-Ukraine conflict could show up in consumer prices. Russia is the largest wheat exporter in the world. As the Times notes, Russia and Ukraine make up 30 percent of global wheat exports, and Ukraine is also a major exporter of corn, barley, and vegetable oil. Disruptions to any of that could lead to disruptions in the commodities markets, therefore pushing up prices eventually at the grocery store. The conflict has caused wheat prices to surge. Bloomberg reported in February that the Biden administration isn’t yet going to impose sanctions on Russia that would impact aluminum, which would throw a wrench in the global supply, though aluminum and metal prices have already gone up.

“It’s a combination of a set of commodities that are being produced either in Ukraine or Russia that have been affected,” Daco said. He warned that if further sanctions are imposed on Russia, it could affect aluminum and commodities prices even more. “It’s a wide spectrum of agricultural, energy, and other commodities.” On Tuesday, Russian President Vladimir Putin signed a decree banning the exports of some commodities, which could have major global ramifications.

I took a brief moment from the news in the last hour … Big mistake.

This will have a dramatic impact on inflation, global value chains, growth and could cause a global recession. https://t.co/SP8YnMc9Q7

— Elina Ribakova (@elinaribakova) March 8, 2022

Reuters reported that the White House has warned the microchip industry about the possibility that Russia will curb access to some of the materials it sources from Ukraine and Russia and to look into diversifying the supply chain. A chip shortage and kinks in the semiconductor supply chain have contributed to higher prices and challenges across a number of industries, including cars and phones.

To be sure, there’s still plenty of uncertainty around what will happen in the Russia-Ukraine conflict and its economic consequences. Brusuelas told MarketWatch in February that the inflationary pressures depend “on the severity of sanctions and what happens on the ground.” The US and Europe have hit Russia with severe sanctions that will devastate the Russian economy and likely have a widespread impact on economic conditions around the world. In other words, economic uncertainty, including inflation, is probably not going away anytime soon.

In the United States, this will be a headache for the Federal Reserve, which is already on track to likely start to raise interest rates in an effort to combat inflation and otherwise roll back some supports for the economy.

“Energy prices mean that inflation is going to stay well above the Fed’s target in 2022, and that’s going to stiffen the Fed’s resolve to normalize monetary policy this year,” Bill Adams, chief economist for Comerica Bank, told Vox. “Inflation was drastically above the Fed’s target in 2021 and had looked like it was about to slow in 2022, but the surge in energy prices caused by the invasion is going to keep inflation higher for longer.”

Adams did, however, note that the US economy is quite strong at the moment, despite inflation. Jobs are coming back, and supply chain problems are being worked out.

“The big picture is that the US economy is strong and is well-positioned to absorb a shock like higher energy prices or disruptions to commodity supply from the Russia-Ukraine war,” he said. “We’re in a better position to absorb this shock than, for example, in 2006-2007 when energy prices were jumping but consumer balance sheets were much more stressed than they are today.”

Still, for Americans already navigating inflation, the current crisis is likely going to push prices up before they come down.

Update, March 8, 2022: This story was updated to include new economic developments stemming from the war in Ukraine.

The 50-year anniversary of the OPEC oil shock is being echoed by “something similar but substantially worse — the 2022 Russia supply shock,” says Credit Suisse’s Zoltan Pozsar.

Fears of a recession and a 1970s-style stagflation economy continue to grip Wall Street and investors this week, as multiple reports show that recession signals have intensified. With oil and commodity prices surging, Reuters reports that investors are “recalibrating their portfolios for an expected period of high inflation and weaker growth.”

While Wall Street Fears Stagflation, Analyst Believes ‘Global Markets Will Collapse’ This Year

This week there’s been a slew of headlines indicating that fears of a 1970s-style stagflation economy have risen and economic fallout is coming soon. Three days ago, Reuters’ author David Randall noted that U.S. investors are scared of a hawkish central bank, oil prices surging, and the current conflict in Ukraine. Randall spoke with Nuveen’s chief investment officer of global fixed income, Anders Persson, and the analyst noted stagflation isn’t here just yet, but it is getting near that point.

“Our base case is still not 1970s stagflation, but we’re getting closer to that ZIP code,” Persson said.

On Saturday, Bitcoin.com News reported on the skyrocketing energy stocks, precious metals, and global commodities breaking market records. The same day, the popular Twitter account Pentoshi tweeted about a pending “greater depression.” At the time of writing, the tweet was retweeted 69 times and has close to a thousand likes. Pentoshi told his 523,500 Twitter followers:

The most exciting thing this year. Will be global markets collapsing. Any market that trades above 0 will be too high. They will call this: ‘The greater depression’ which will be 10x worse than the Great Depression.

US Treasury Yield Curve Highlights ‘Recession Concerns Showing up More Prominently’

The following day, Reuters’ author Davide Barbuscia detailed that “recession concerns are showing up more prominently in the U.S. Treasury yield curve.” Data from Barbuscia’s report stresses that the “closely watched gap between yields on two- and 10-year notes stood at its narrowest since March 2020.”

Numerous financial publications are highlighting how rising oil and commodity prices are typically associated with a pending recession. Furthermore, recent filings indicate that Warren Buffett’s Berkshire Hathaway obtained a $5 billion stake in Occidental Petroleum. Berkshire Hathaway has also doubled the firm’s exposure to Chevron as well.

What do you think about the reported signals that show a recession or 1970s stagflation is looming over the economy? Let us know what you think about this subject in the comments section below.

Who’s blocking progress on climate change? Fossil fuel companies and politicians in rich, high-emitting countries are the biggest obstructionists—the ones climate activists are rightly targeting with political campaigns, investigations, and direct actions. But as two recent reports have made clear, there’s another group climate watchers need to consider if the world is to avoid catastrophe: asset managers.

Asset management firms manage and invest the pooled funds of individual and institutional investors like billionaires, pension funds, and colleges. The world’s three largest asset managers (BlackRock, Vanguard, and UBS) alone control $21 trillion, roughly equivalent to the entire U.S. economy in 2017 and nearly twice as much as the entire world’s hedge fund, private equity, and venture capital industries combined. And asset management firms own a piece of virtually every industry: The “Big Three” of BlackRock, Vanguard, and State Street own more than 20 percent of shares in the average publicly traded S&P500 company and are also big players in private equity.

These companies have quietly taken up a central role in our economic and political life. The Big Three cast more than 25 percent of votes at corporate shareholder meetings, meaning they “exercise something akin to state authority over the largest corporations that account for the vast bulk of economic activity in … the world economy,” as investment strategy analyst Anusar Farooqui put it last year. It’s not just corporate governance, either: Major political decisions around the construction of crucial public infrastructure like the building of roads and hospitals have been structured in order to eliminate risk for asset managers and their clients as part of “public-private partnerships.” In 2020, professor and finance law expert William Birdthistle went as far as to call BlackRock a “fourth branch of government,” after the U.S. Federal Reserve again enlisted it to prop up the entire corporate bond market.

If climate justice is to succeed, it will involve taking on this new branch of government. A new report by Friends of Earth U.S. reveals that the Big Three asset managers collectively own more than 27 percent of shares in fossil fuel giants Chevron, ExxonMobil, and Conoco Phillips and over 30 percent of major agribusiness companies like Archer-Daniels-Midland, making them among the largest shareholders in the two industries most responsible for the majority of greenhouse gas emissions driving the climate crisis.

These faceless financial giants are not just funneling money into the companies causing the crises themselves; they’re also profiting off unjust responses to these crises. An earlier investigation by Jordi Calvo Rufanges finds that these mammoth asset managers are among the largest financiers of the global arms trade. The Friends of the Earth investigation adds that the asset managers are major investors in the companies that run private prisons and migrant detention centers and provide the drone and biometric technology that are revolutionizing the increasingly militarized border violence against displaced peoples around the world. All told, asset management companies own over $650 billion of shares in the top fossil fuel, agribusiness, border security, and surveillance companies surveyed by the Friends of the Earth report.

This adds up to a grim picture for climate justice. The business models propped up by these investments disproportionately impact low-income communities of color in the global north and global south—people who have contributed little to global cumulative emissions yet who are endangered by fossil fuel extraction’s sacrifice zones and industrial agriculture’s pollution, not to mention being disproportionately affected by flooding, rising food prices, and more. Their needs are routinely ignored: The same countries enthusiastically opening their doors for Ukrainian refugees spent the last decade enthusiastically closing them to refugees from Africa and the Middle East, while promoting the very high-tech, militarized borders and detention centers that asset managers are investing in.

No wonder climate change represents an “opportunity” for asset managers like BlackRock CEO Larry Fink. In 2021, Fink took the opportunity of BlackRock’s annual letter to CEOs—something of an unofficial State of the Union for the global nation of capital—to remind chief executives that “there is no company whose business model won’t be profoundly affected by the transition to a net-zero economy.” The largest asset managers hold major stakes in every industry and asset class on the planet and possess the size and reach to make sure that they profit off both the industries causing the problems and the violent, unequal “solutions” they fund.

Meanwhile, the world is decades late and a trillion dollars short on less dystopian responses to climate crisis: There are major gaps in available financing for a global shift to renewable energy that would prevent the worst impacts, as well as for adapting to the impacts that are already here. The new IPCC report is clear: “Half measures are no longer an option.”

Some might expect that asset managers would be a force for progress on climate crisis, since the diversity of asset managers’ investments makes them exposed to a wider range of risks than most investors are. Climate crisis destroying the world would eventually wreak havoc on portfolio returns, so shouldn’t the firms managing those portfolios have a direct financial interest moving climate policy forward?

But this is mistaken: You could fit an oil tanker in the space between what’s good for asset management companies and what’s good for the world. Asset management companies are paid fees for each dollar they manage—they profit by managing as much money as possible, not by managing it well. Each asset management company is then motivated to invest well, but only so well that its clients don’t take their funds elsewhere, encouraging companies to chase big short-term returns or face losing ground to competitors.

On top of that, what’s good for portfolios, especially in the short term, isn’t necessarily good for people: The very same rising asset valuations that make housing a lucrative investment and an attractive part of a portfolio is also what entices corporate landlords to send rents skyrocketing nationwide, making housing unaffordable and unavailable for the vast majority of people across the planet. Moreover, the people who will be detained and confronted at militarized borders are likely not clients of BlackRock or Vanguard.

Unsurprisingly, asset managers have not used their considerable power to promote genuine climate sustainability or justice-promoting responses to the climate crisis. Instead, they have routinely voted against or abstained on shareholder resolutions that would support establishing serious climate targets or delinking supply chains from deforestation to climate targets. All the while, they have attempted to greenwash their continued investment patterns with “green investment funds,” the commanding majority of which are incompatible with global climate targets while fitting squarely into the goals of investors and financial capital. Tariq Fancy, former chief investment officer of Sustainable BlackRock, publicly called out the financial services industry for “duping the American public” and labeled sustainable investing as a “dangerous placebo that harms the public interest.”

Climate justice will require a serious course correction. We need comprehensive regulatory strategies to level the playing field between public institutions and unaccountable private capital and the asset manager behemoths managing their investments: including wealth taxes on corporate stock, as suggested by economists like Emmanuel Saez and Gabriel Zucman, alongside global tax reform.

But these can only mitigate the deeper problem for climate justice, which is that injustice has been and will likely continue to be profitable. Our continued reliance on the private sector for climate financing all but guarantees that profiteering off misery will continue. Only an energy democracy that takes crucial climate decisions out of the hands of private investors and into publicly accountable hands can tackle this core problem. That means building robust public systems of investment without “partnering” with private capital. Fortunately, scholars and activists have long discussed many existing options. Policymakers just need to implement them.

Whether by building new institutions like national investment authorities or finding ways to make our existing systems of spending more democratically responsive, a more transformative political shift to public investment is necessary. We should get started yesterday.

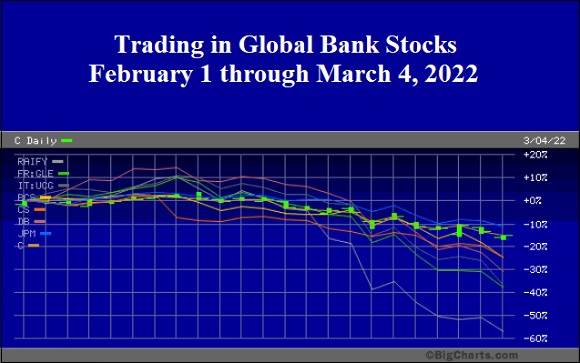

The Big Question on Wall Street Is Which Banks Owe $41 Billion on Credit Default Swaps on Russia

By Pam Martens and Russ Martens: March 7, 2022 ~ There is a known $41 billion in Credit Default Swaps (CDS) on Russian debt. There is likely many billions more in unknown amounts. There are also billions more in Credit Default Swaps on state-owned Russian corporate debt and non state-owned Russian corporate debt. In addition to Wall Street not knowing which global banks and other financial institutions are on the hook to pay out on the Credit Default Swap protection they sold in case of a Russian sovereign debt default (or Russian corporate debt default), there is also approximately $100 billion of Russian sovereign debt (whose default is looking more and more likely) sitting on the balance sheets of foreign banks. Put it all together and you have the makings of a replay of the 2008 banking crisis when banks backed away from lending to each other because they didn’t know … Continue reading →

The committee alleges that Trump and his allies engaged in a “corrupt scheme to obstruct the counting of Electoral College ballots and a conspiracy to impede the transfer of power.”

“What do you get when you restore government as a force for the common good?” asked Rep. Jamie Raskin. “An unprecedented economic recovery with 7.4 million jobs created in just 13 months.”

Sanctions on Russia highlight Beijing’s efforts to internationalise the renminbi